Reliable ClaimCenter-Business-Analysts Test Experience, Exam Dumps ClaimCenter-Business-Analysts Free

Wiki Article

What's more, part of that FreeCram ClaimCenter-Business-Analysts dumps now are free: https://drive.google.com/open?id=1xgj9_N6UbS-g1cVDe9Q-qtK5HSoR7P8O

People who appear in the test of the ClaimCenter Business Analyst - Mammoth Proctored Exam (ClaimCenter-Business-Analysts) certification face the issue of not finding up-to-date and real exam dumps. FreeCram is here to resolve all of your problems with its actual and latest Guidewire ClaimCenter-Business-Analysts Questions. You can successfully get prepared for the ClaimCenter Business Analyst - Mammoth Proctored Exam (ClaimCenter-Business-Analysts) examination in a short time with the aid of these test questions.

Guidewire ClaimCenter-Business-Analysts Exam Syllabus Topics:

| Topic | Details |

|---|---|

| Topic 1 |

|

| Topic 2 |

|

| Topic 3 |

|

>> Reliable ClaimCenter-Business-Analysts Test Experience <<

Advantages Of Guidewire ClaimCenter-Business-Analysts Practice Test Software

The Guidewire ClaimCenter-Business-Analysts certification exam is one of the top-rated and valuable credentials in the Guidewire world. This Guidewire ClaimCenter-Business-Analysts exam questions is designed to validate the candidate's skills and knowledge. With ClaimCenter Business Analyst - Mammoth Proctored Exam exam dumps everyone can upgrade their expertise and knowledge level. By doing this the successful ClaimCenter-Business-Analysts Exam candidates can gain several personal and professional benefits in their career and achieve their professional career objectives in a short time period.

Guidewire ClaimCenter Business Analyst - Mammoth Proctored Exam Sample Questions (Q44-Q49):

NEW QUESTION # 44

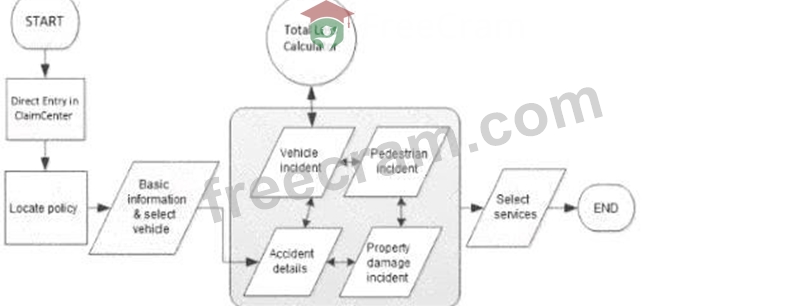

Whenever the Total Loss Calculator determines that a vehicle is a total loss, Succeed Insurance wants to create a custom history event with the exposure name and total loss score.

Which step in the claim setup process flow must be completed before the history event can be created?

- A. Add a new step before the Total Loss Calculator to create the history event.

- B. Add a new step after the Total Loss Calculator to create the history event.

- C. Add a new step after the Vehicle Incident step to create the history event.

- D. Add a new step before the Vehicle Incident step to create the history event.

Answer: B

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In Guidewire ClaimCenter workflow analysis and configuration, defining the correct sequence of operations is critically dependent on Data Availability and Data Dependency.

The specific requirement here dictates that the custom history event must capture theTotal Loss Score. In the context of the ClaimCenter object model and process flow, the Total Loss Score is anoutputvalue generated specifically by theTotal Loss Calculatorengine. Before this calculator runs, the score attribute is effectively null or non-existent.

Therefore, to satisfy the business requirement, the step that writes the history event must be placedafterthe step that generates the data it needs to record.

* Process Logic:If the Business Analyst were to place the history event creation stepbeforethe Total Loss Calculator (Option B) orbeforethe Vehicle Incident (Option D), the system would attempt to write a record containing a score that has not yet been calculated. This would result in either a system error or a history event with a blank/zero value, failing to meet the business requirement.

* Dependency Chain:The workflow dependency is: Vehicle Data Entry -> Total Loss Calculation -> Score Generation -> History Event Creation.

* Implementation Note:In a typical Guidewire implementation, this logic is often handled via "Event Fired" rules or specific "Exit Points" in the workflow. The system waits for the confirmation that the Total Loss calculation service has successfully returned a result. Once that transaction is committed and the score is persisted on the Vehicle or Exposure entity, the subsequent rule to generate the History Event can trigger successfully.

Consequently,Option Cis the only viable placement in the process flow. It ensures that the prerequisite action (calculation) is complete and the required data payload (the score) is available for the subsequent action (logging the history event).

NEW QUESTION # 45

To optimize business process workflow, an insurer has spent a great deal of effort on estimating the amount of effort required to complete various types of work... They are also aware that certain situations may require specialized expertise and want to incorporate this in their decision making.

All claims and exposures are entered using only the ClaimCenter new claim wizard. Once entered, the work should be automatically distributed fairly to those properly suited, as determined by the company's knowledge of each worker's skill set.

Which two assignment mechanisms, alone or together, will achieve their goal? (Choose two.)

- A. FNOL queues

- B. Supervisor assignment

- C. Round-robin

- D. User attribute

- E. Weighted workload

Answer: D,E

Explanation:

To meet the dual requirements of "specialized expertise" and "fair distribution based on effort," the Business Analyst should utilize User Attributes and Weighted Workload assignment rules.

* User Attributes (Option B):This feature handles the "specialized expertise" requirement.

Administrators can tag users with specific attributes (e.g., "Bilingual," "Heavy Equipment Expert,"

"Litigation Specialist"). Assignment rules can then be configured to filter the pool of potential assignees toonlythose who possess the matching attribute for the specific claim type.

* Weighted Workload (Option D):This feature handles the "fair distribution" and "amount of effort" requirement. Unlike Round-robin (which treats all claims as equal), Weighted Workload assigns a

"weight" (effort points) to the claim and tracks the "load factor" (current capacity) of the user. The system assigns the new work to the user with the lowest relative workload, ensuring that adjusters handling difficult, high-effort claims are not overwhelmed with the same volume as those handling simple claims.

Why other options are incorrect:

* Round-robin (A):Distributes work purely cyclically (1-2-3-1-2-3) without regard for the user's current workload or the complexity of the claim.

* FNOL Queues (C):This is a "pull" mechanism where work sits in a bucket until someone grabs it, rather than the "automatic distribution" (push) requested.

* Supervisor Assignment (E):This is manual, not automatic.

NEW QUESTION # 46

Succeed Insurance requires that a new 'Driver under 18?' field be added to the vehicle incident screen for personal auto claims to indicate whether or not the driver of the vehicle was a minor when the loss occurred.

The field will be set by calculating the driver's age using the date of loss and the driver's date of birth.

There are two validation requirements:

* The field must be set if the 'Date of Birth' field for the driver is not null.

* No payments can be made for collision exposures if the 'Date of Birth' field for the driver of the vehicle is null.

A Business Analyst (BA) documents the validation requirements in the validation tab of the User Story Card

'Adjudicate - Update Maintain Vehicle Incident for Personal Auto Claims' as shown in the exhibit.

What information in the two validation examples is either missing or incorrectly documented? (Choose two.)

- A. The second requirement is missing a requirement number, and the rule condition should check for a policy type of personal auto.

- B. The first requirement includes information on how to set the new 'Driver under 18?' field in the Rules column, which is not needed.

- C. The first requirement does not need a value in the LOB column since the rule condition provides a test for the policy type.

- D. The second requirement is missing the name of the DV or LV file where the warning or error message will display when the validation fails.

- E. The first requirement is missing the name of the DV or LV file for the new field, and an error or warning message should be provided.

Answer: A,D

Explanation:

The User Story Card exhibit contains several documentation errors when compared to standard Guidewire requirements gathering best practices and the specific scenario provided.

* Missing Requirement Number and Logic Gap (Option C):

* Traceability:In the second row of the exhibit (the payment validation rule), the "Requirement Number" column is completely blank. Traceability back to the original requirements document is mandatory for all entries.

* Logic Precision:The requirement explicitly states that the rule applies to"personal auto claims"

. However, the logic documented in the "Rules" column (If Exposure Type = VehicleDamage Then Block...) doesnotcheck the Policy Type. It relies solely on the Exposure Type, which could exist on Commercial Auto policies as well. To accurately reflect the business requirement, the condition If PolicyType = Personal Auto must be added (similar to how it was done in the first row).

* Missing DV/LV Context for Validation (Option D):

* UI Anchoring:The second requirement is a validation rule that triggers an error ("Driver's Date of Birth is required..."). For the system to highlight the specific field on the screen (the "Driver Date of Birth" widget) when the error occurs, the rule must be associated with the specificDetail View (DV)orList View (LV)where that field resides (e.g., VehicleIncidentDV). The exhibit lists

"Not Applicable" in the "Name of DV or LV" column. This is incorrect because providing the DV name ensures the error message is displayed contextually next to the field rather than as a generic page-level error, improving the user experience.

Why other options are incorrect:

* Option A:The LOB column is used for filtering, reporting, and release management. Even if the rule logic checks the policy type, the LOB column is required metadata and should not be removed.

* Option B:While the first requirement (the calculation) lacks a DV name (which it should have), it is a Business Rule(assignment), not a validation. Therefore, it doesnotgenerate an error or warning message for the user, so the second part of Option B is incorrect.

* Option E:The "Rules" column is exactly where the calculation logic (Date of Loss - Date of Birth) belongs. The developer needs this information to implement the automation.

NEW QUESTION # 47

An auto claim is owned by Adjuster1. The Customer Service Representative (CSR) that created the claim owns one follow-up activity on the claim. An Injury Specialist owns an injury exposure on the claim. All these persons are members of Auto Team 1.

The Team Lead determines that Adjuster1 is overworked and reassigns the claim to Adjuster2, a member of Auto Team 2.

Which three people now have access to the claim? (Choose three.)

- A. Special Investigations Unit

- B. Adjuster2

- C. CSR

- D. Injury Specialist

- E. Adjuster1

- F. The Claimant

Answer: B,C,D

Explanation:

250 to 350 words From Exact Extract of Guidewire ClaimCenter Business Analyst documentation:

In Guidewire ClaimCenter, access to a claim file is determined by Access Control Lists (ACLs), which are dynamically updated based on user roles and ownership. A user is granted access to a claim if they own the claim itself, or if they own a sub-object within that claim, such as an Activity or an Exposure.

* Adjuster2 (Option E):Upon reassignment, Adjuster2 becomes the newClaim Owner. The owner of the claim record always has full view and edit access to the claim.

* CSR (Option C):The CSR retains ownership of a specificActivity(the follow-up task). In the ClaimCenter security model, owning an open activity on a claim grants the user "view" access to the parent claim so they can perform the necessary work to complete their task. Reassigning the claim header does not automatically reassign the activities owned by other users.

* Injury Specialist (Option D):This user owns anExposure(a distinct financial sub-record for a specific coverage feature). Similar to activities, owning an exposure grants access to the parent claim. The reassignment of the main claim file from Adjuster1 to Adjuster2 does not strip the Injury Specialist of their ownership of the specific injury exposure.

Why Adjuster1 loses access:Adjuster1 was the previous owner. Once ownership is transferred to Adjuster2 (who is in a different group, "Auto Team 2"), Adjuster1 no longer meets the criteria for ownership access.

Unless Adjuster1 is explicitly added to the ACL manually or has "Super User" privileges (not stated), they lose the automatic access rights associated with being the owner.

NEW QUESTION # 48

A performing arts organization operates nationwide and is responsible for setting up stages for musical acts and concerts. The organization requires specific insurance coverage for its gear and equipment, including audio systems, lighting, cameras, and control boards. Succeed Insurance wants to optimize claim intake, processing, and reporting for this organization.

Which modifications should be made to ClaimCenter's base product line of business (LOB)?

- A. Add newLossTypecode(s) andPolicyTypecode(s) to the LOB model to handle the organization's coverage needs.

- B. Add relevantCoverageTypecode(s),Coverage Subtypecode(s), and mapExposureTypecode(s) to support the new coverage.

- C. Add newCoverage Subtypecode(s) with detailed information for eachExposureTypecode to the existing LOB model.

- D. The existing ClaimCenter standard LOB model can meet the company's objectives without modifications.

Answer: B

Explanation:

According to the Guidewire ClaimCenter Business Analyst documentation, ClaimCenter's line of business (LOB) framework is intentionally designed to support extensibility through configuration rather than structural changes to core policy or loss classification elements. When an insurer needs to support specialized insured property-such as professional audio, lighting, and staging equipment-the recommended approach is to enhance the coverage configuration.

ClaimCenter models policy coverage using a hierarchy ofCoverageTypeandCoverage Subtypetypelists.

CoverageType codes represent high-level coverage categories defined by the policy, while Coverage Subtype codes allow insurers to further refine and classify coverage details. These coverage elements are then associated withExposureTypecodes, which drive claim processing behavior such as exposure creation, reserving, payment handling, and reporting.

By adding appropriate CoverageType and Coverage Subtype codes for equipment and gear coverage and mapping them to ExposureType codes, ClaimCenter can automatically create accurate exposures during claim intake. This approach ensures adjusters can efficiently process claims while maintaining consistent workflows and financial controls. It also supports meaningful analytics and reporting without altering the base product structure.

The Guidewire documentation advises against introducing newLossTypeorPolicyTypecodes unless the insurer is defining an entirely new policy or loss classification. LossType codes describe how a loss occurred (for example, theft or accidental damage), not the nature of the insured property. PolicyType changes are similarly broad and unnecessary for extending coverage within an existing LOB.

Therefore, optionBaligns with Guidewire best practices by extending ClaimCenter's coverage and exposure configuration to meet the organization's needs while preserving the integrity of the standard LOB model.

NEW QUESTION # 49

......

With both ClaimCenter-Business-Analysts exam practice test software you can understand the ClaimCenter Business Analyst - Mammoth Proctored Exam (ClaimCenter-Business-Analysts) exam format and polish your exam time management skills. Having experience with ClaimCenter-Business-Analysts exam dumps environment and structure of exam questions greatly help you to perform well in the final ClaimCenter-Business-Analysts Exam. The desktop practice test software is supported by Windows. Our web-based practice exam is compatible with all browsers and operating systems.

Exam Dumps ClaimCenter-Business-Analysts Free: https://www.freecram.com/Guidewire-certification/ClaimCenter-Business-Analysts-exam-dumps.html

- ClaimCenter-Business-Analysts Test Guide: Guidewire Certified Professional - ClaimCenter-Business-Analysts Exam Torrent - ClaimCenter-Business-Analysts Training Materials ???? ➽ www.easy4engine.com ???? is best website to obtain ⇛ ClaimCenter-Business-Analysts ⇚ for free download ????Latest ClaimCenter-Business-Analysts Dumps Book

- 2026 Guidewire ClaimCenter-Business-Analysts Fantastic Reliable Test Experience ???? Search for ▛ ClaimCenter-Business-Analysts ▟ and easily obtain a free download on ( www.pdfvce.com ) ????Test ClaimCenter-Business-Analysts Questions Answers

- Test ClaimCenter-Business-Analysts Questions Answers ???? ClaimCenter-Business-Analysts Valid Dumps Files Ⓜ ClaimCenter-Business-Analysts Demo Test ???? The page for free download of 【 ClaimCenter-Business-Analysts 】 on 《 www.testkingpass.com 》 will open immediately ????ClaimCenter-Business-Analysts Dumps

- Excellent Guidewire Reliable Test Experience – 100% Pass-Rate Exam Dumps ClaimCenter-Business-Analysts Free ???? Open ⇛ www.pdfvce.com ⇚ and search for ➥ ClaimCenter-Business-Analysts ???? to download exam materials for free ????Premium ClaimCenter-Business-Analysts Exam

- ClaimCenter-Business-Analysts Test Guide: Guidewire Certified Professional - ClaimCenter-Business-Analysts Exam Torrent - ClaimCenter-Business-Analysts Training Materials ✔️ Search for ➤ ClaimCenter-Business-Analysts ⮘ and obtain a free download on ▶ www.testkingpass.com ◀ ????Premium ClaimCenter-Business-Analysts Exam

- 100% Pass Guidewire - ClaimCenter-Business-Analysts - ClaimCenter Business Analyst - Mammoth Proctored Exam Latest Reliable Test Experience ☕ Immediately open ➽ www.pdfvce.com ???? and search for ➽ ClaimCenter-Business-Analysts ???? to obtain a free download ????ClaimCenter-Business-Analysts Latest Guide Files

- ClaimCenter-Business-Analysts Test Guide: Guidewire Certified Professional - ClaimCenter-Business-Analysts Exam Torrent - ClaimCenter-Business-Analysts Training Materials ???? ▷ www.examcollectionpass.com ◁ is best website to obtain ➥ ClaimCenter-Business-Analysts ???? for free download ????Premium ClaimCenter-Business-Analysts Exam

- 100% Pass Guidewire - ClaimCenter-Business-Analysts - ClaimCenter Business Analyst - Mammoth Proctored Exam Latest Reliable Test Experience ???? Search for “ ClaimCenter-Business-Analysts ” and download it for free on ➤ www.pdfvce.com ⮘ website ↕ClaimCenter-Business-Analysts Latest Test Simulator

- ClaimCenter-Business-Analysts Latest Cram Materials ???? ClaimCenter-Business-Analysts New Practice Materials ???? Discount ClaimCenter-Business-Analysts Code ???? Download ⮆ ClaimCenter-Business-Analysts ⮄ for free by simply searching on “ www.validtorrent.com ” ????ClaimCenter-Business-Analysts Latest Cram Materials

- Test ClaimCenter-Business-Analysts Questions Answers ???? ClaimCenter-Business-Analysts Dumps ???? New ClaimCenter-Business-Analysts Exam Book ???? Open ⇛ www.pdfvce.com ⇚ and search for ➡ ClaimCenter-Business-Analysts ️⬅️ to download exam materials for free ????New ClaimCenter-Business-Analysts Braindumps Free

- Premium ClaimCenter-Business-Analysts Exam ???? ClaimCenter-Business-Analysts Valid Dumps Files ???? ClaimCenter-Business-Analysts Reliable Exam Cram ???? Open ➤ www.validtorrent.com ⮘ enter ⇛ ClaimCenter-Business-Analysts ⇚ and obtain a free download ????ClaimCenter-Business-Analysts Latest Test Simulator

- pruebas.alquimiaregenerativa.com, faymncj753590.idblogmaker.com, jemimahymn386852.wikidank.com, lawsonromc659561.blogitright.com, margietake800915.verybigblog.com, deweyboql036834.levitra-wiki.com, sidneywuao562301.glifeblog.com, tripsbookmarks.com, nelsonrfde973937.wikievia.com, www.stes.tyc.edu.tw, Disposable vapes

2026 Latest FreeCram ClaimCenter-Business-Analysts PDF Dumps and ClaimCenter-Business-Analysts Exam Engine Free Share: https://drive.google.com/open?id=1xgj9_N6UbS-g1cVDe9Q-qtK5HSoR7P8O

Report this wiki page